SMB SOLUTIONS

Let us simplify payments so you can focus on your patients.

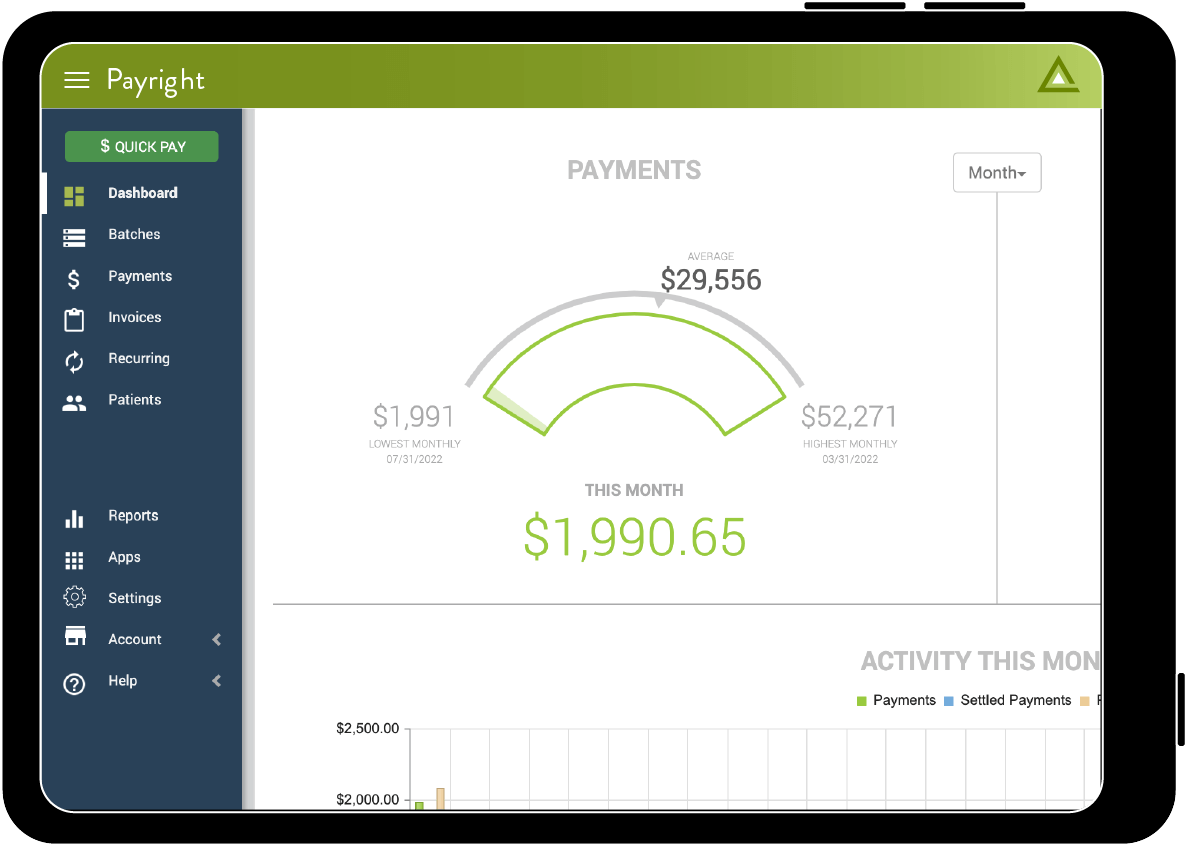

Priority makes it possible for healthcare and home care providers to collect patient payments faster while lowering overall costs for merchant services and ACH processing—and syncs payments to patient records effortlessly. When you accept payments with PayRight, you drive significant saving and revenue to your bottom line.

Who We Help

Non-Medical Home Care Providers

- • Our pre-sales claim benefit analysis provides you with a comprehensive report that details pertinent policy information, daily max benefit, plan of care, remaining balance, requirements for eligibility, and much more.

- • Revenue management to ensure your claim is compliant, clean, and submitted with all the appropriate back up.

- • Advance funding allows you to take an advance against the claim for either 40% or 60% of the claim value.

- • PayRight has clients who use nearly every type of scheduling software.

Home Care Franchisors

- • Provide options to your franchisees for both self-pay and third-party payment (TPP) collection.

- • Offer operational financing to allow agencies to grow based on TPP billing.

- • Access our certified billing experts and full-service TPP billing center.

Veteran’s Administration Providers

- • PayRight can help verify authorizations and create and submit a clean and compliant claim to streamline reimbursement from the VA.

Agency Management Software Providers

- • Choose from a variety of APIs and functionality.

- • Embed our workflow in your application or create your own.

- • Accept a wide variety of payment options – backed by the financial stability of one of the largest non-bank processors in the US.

Banks and Financial Services Companies

- • Differentiate your healthcare offering.

- • Provide increase payments volume.

- • Whitelabel our product suite to deliver a custom solution.

Practice Management

- • Choose from a variety of APIs and functionality.

- • Embed our workflow in your application or create your own.

- • Accept a wide variety of payment options – backed by the financial stability of one of the largest non-bank processors in the US.

KEY FEATURES

Healthcare Providers

Keep Card or Account on File Details Securely Vaulted

Create Invoices, Automate Recurring Billing, and Offer Payment Plans with our HIPAA, PCI-DSS and EMV compliant solutions and optional MX™ Account Updater.

Customize a Contactless Payment Experience

Give patients options to pay at point of service or over time, online or with a mobile device. Add an EMV card reader or your logo to our patient-facing bill payment portal for fully optimized patient engagement.

Sync Payments with Leading EHRs and Quickbooks Online

Minimize dual data entry and free your staff to focus on patients not paperwork.

Get Paid Faster and Reconcile with Ease

Receive next day funding and access real-time reports online or via API.

KEY FEATURES

Home Care Offices

Expert Resources

Dedicated team of LTCi, VA and payment experts.

Proven Experience

LTCi, VA, & private pay experience.

Focused Technology

Home care billing & payment automation tools.

We can even take care of direct patient pay and balance billing.

We can even take care of direct patient pay and balance billing.

Solid Foundation

Your agency receives payment advances weekly to ensure cash flow. Financial backing of a leading payment processor.

$1,500 in Monthly

Saving

Saving

26% Reduction in

Processing Fees

Processing Fees

CONTACT

Interested?

Our experienced payment advisors specialize in working with businesses just like yours to create innovative solutions based on your specific needs.

Support